|

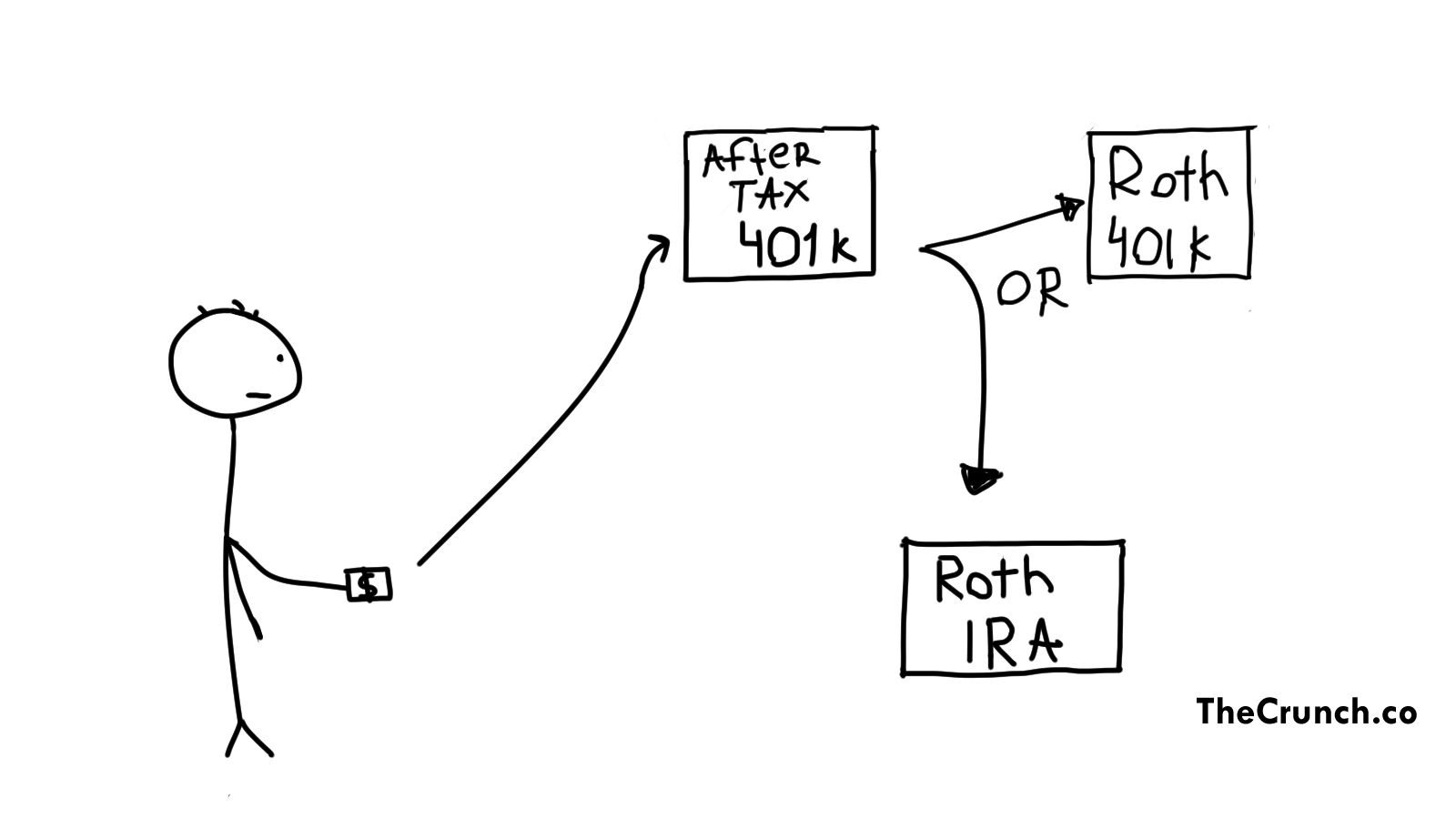

Mega Backdoor Roth Read time: 3 minutes Read on: my website Roth accounts are extremely beneficial during retirement. You will pay $0 tax on investment gains when you withdraw. So, getting as much money as you can into the Roth accounts should be the goal. Roth accounts have limits. For example, Roth IRA is capped at $7,000 per year (high earners need to use Backdoor Roth strategy to contribute) or 401k is at $23,000 per year. But what if you wanted to contribute more? That’s where Mega Backdoor Roth comes into play… Mega Backdoor Roth Mega Backdoor Roth is a strategy that allows funding Roth accounts far in excess of normal limits. It’s a 2 step process:

This strategy is only available through the employer’s 401k, so you need to ask whether your plan allows it. Here is the email I personally sent to my 401k plan asking whether it’s available:

Unfortunately, if your employer doesn’t allow it, this strategy wouldn’t be available. The rules will usually vary from plan to plan, so it’s also important to check your Summary Plan Description. Where should I roll? Step 2 requires you to roll the after-tax contribution to either Roth 401k or Roth IRA So, which is better? First of all, your plan might only allow you to roll into a Roth 401k, so it’s important to check that first. But if you have both options available, here are the benefits of each: Roth 401k – allows minimizing taxable earnings by automatic conversion and might be easier to set up Roth IRA – offers a greater variety of investment options and has flexibility of withdrawals (can withdraw contributions penalty free at any time). In my opinion, rolling into a Roth IRA is a better option. Total limits The total limit to contribute to the employer plan is $69,000 in 2024. So if you are contributing $23,000 to the 401k, receiving a $5,000 match, you can contribute $41,000 extra to the Roth account! Advantages of Mega Backdoor strategy Large contributions to Roth account (ability to contribute $40,000+) Further growth is all tax free Protected from creditors under ERISA Earnings When you contribute to after-tax (step 1), the amount is automatically invested. Then, when you roll the balance into a Roth IRA (step 2), you might have some earnings. These earnings are taxable income. To reduce the taxable amount, do steps 1 and 2 as soon as possible. Some plans might offer automatic roll, or the ability to invest in a Money Market Fund to minimize earnings. Some employers might issue separate checks to split the contributions and earnings. In that regard, you might put the after-tax contributions to a Roth IRA and earnings into a Traditional IRA and pay no tax. But be careful, as contributing to a Traditional IRA might impact your Backdoor Roth strategy, if you are using one. Example Say you have $5,000 in your Roth IRA, and contributed $10,000 to the after-tax 401k account (step 1). You then roll it into a Roth IRA (step 2). Assume there was $100 in earnings earned between step 1 and 2. You can roll $10,100 into the Roth IRA and pay taxes on the $100. Your total Roth IRA account will be $15,100; OR Roll $100 into the Traditional IRA (no tax impact), and roll $10,000 into the Roth IRA. Your total Roth IRA account will be $15,000. In summary, this is how it basically works:

I hope you enjoyed this one. If you have any questions, hit that “Reply” See you next Saturday. MC, CPA |